- Home

- >

- GHF Blog Page and...

GHF Blog Page and Post Template

Join Cover Georgia in celebrating Juneteenth

As we approach Juneteenth, let’s celebrate the progress that has been made towards racial equality in the U.S., and pause to assess the gaps and inequities that still affect the Black community. At Cover Georgia, we are and know Black Georgians remain uninsured and stuck in our state’s coverage gap. These individuals work hard earning low wages, caring for loved ones, or managing chronic health conditions while in a vulnerable position: unable to afford private insurance and ineligible for Medicaid.

13% of Black Georgians are uninsured (3 percentage points higher than white Georgians), and Black workers make up nearly half (46%) of Georgia’s uninsured low-income workers. They are also more likely to have medical debt in collections than white Georgians, partly due to higher uninsured rates.

Because of structural barriers that kept Black people out of good jobs and blocked them from other economic and health opportunities, Black Georgians are more likely to have poor health or have a disability. The unlevel playing field has led to higher rates of chronic conditions (like asthma or diabetes) among Black Georgians. Closing Georgia’s coverage gap is one of the easiest and most powerful actions our state leaders can take to reduce close racial health gaps, support economic mobility, and ensure that health care is a right, not a privilege, for all Georgians.

When Georgia’s gap is closed, an estimated 130,000 Black Georgians and more than 400,000 total Georgians would gain coverage. We need your support to turn this vision into reality. Reach out to your state lawmakers today and urge them to close the coverage gap.

Thank you for sharing your Pathways program experiences with state leaders!

On December 7th, the Georgia Department of Community Health (DCH) held a public forum about the Georgia Pathways to Coverage program. The forum included an opportunity for Georgians to provide feedback about the program.

This Veterans Day, let’s talk about our military heroes and their health. It’s the least we can do for those who sacrificed to serve our country and protect our freedom. But not all Veterans can get the affordable, quality health coverage that they need and deserve – and many are being left behind. As of 2020, across the country, there are more than 1 million Veterans who can’t access the critical physical and mental health care they need. In Georgia, 14,000 veterans cannot access care because our state lawmakers are refusing to close the coverage gap.

As we come together to honor our Veterans and the sacrifices they made to keep us safe, we must urge our elected leaders to bridge the coverage gap by expanding Medicaid. One in every five uninsured Georgia Veterans (and their families) would be able to get the essential health coverage they need to stay healthy and thrive.

Contrary to the wide-spread misconception that all veterans receive health services at the Veteran’s Administration (VA), veterans can be uninsured for several reasons. Those who serve for less than two years, or have an “other than honorable” discharge, may not be eligible for VA benefits. Moreover, eligibility status is prioritized according to a history of service-related injuries and income, among other factors; those in lower priority groups may be denied services. Some veterans may also be unaware of their current eligibility for VA benefits, either because they have never applied, or because they have been rejected in the past.

Medicaid expansion has made a significant difference in communities across the country by allowing residents to secure affordable, high-quality health coverage for themselves and their loved ones.

Veterans and their families deserve access to quality care. It has been reported that less than half of returning Veterans receive the mental health support and treatment they need. With Medicaid, vital mental health services like therapy, inpatient treatment, and prescription medication are all covered. Expanding Medicaid and closing the coverage gap would allow more Veterans and their families to access essential and potentially life-saving mental health services.

Georgia Veterans protected our freedom and served our country. This Veterans Day, let’s honor them by fighting for Medicaid expansion. It’s past time for state lawmakers to act so all Veterans and their families have access to the healthcare they need and deserve.

October is National Breast Cancer Awareness Month

This month, Cover Georgia celebrates Breast Cancer Awareness month and all the Georgia women who are affected by this disease, including Yosha Dotson. We also celebrate that Medicaid covers low-income women fighting Breast and Cervical cancers.

September is recognized as National Suicide Prevention Month

One in four uninsured Georgians who also have low-incomes have a mental illness and/or addiction to drugs or alcohol. Right now, these Georgians often cannot access health services to help them recover except through our state’s limited mental health safety net. These Georgians–our friends and neighbors–could be covered and find better help if Georgia leaders expanded Medicaid to low-income adults.

Since 2010, 10 rural hospitals have closed in Georgia. That puts Georgia fifth in the nation for hospital closures. Rural hospitals in states that have not expanded Medicaid to low-income adults are more likely to close, shutting off access to care for their communities and residents.

Georgia is one of 10 states that has not yet expanded Medicaid. Our leaders’ in action leaves thousands of low-income Georgia adults without health insurance.

Instead of expanding Medicaid, Governor Kemp created a new program called Georgia Pathways to Coverage. This program will cover some low-income adults, but it has a lot of rules and requirements.

To qualify for Pathways, you must meet all of these four requirements:

- Be a U.S. citizen or a qualified permanent resident

- Be between the ages of 19 and 64

- Have an income below the poverty line. (If you don’t know if your income is below the poverty line, use the chart below.)

- Be working or doing other qualifying activities for at least 80 hours per month.

If you are uninsured and meet these requirements, you can apply for Pathways. You can apply online at gateway.ga.gov or by phone at 1-877-423-4746.

If you need assistance with your application, GHF’s enrollment assisters are here to help! Click here to ask for their assistance.

What does this mean for Georgians?

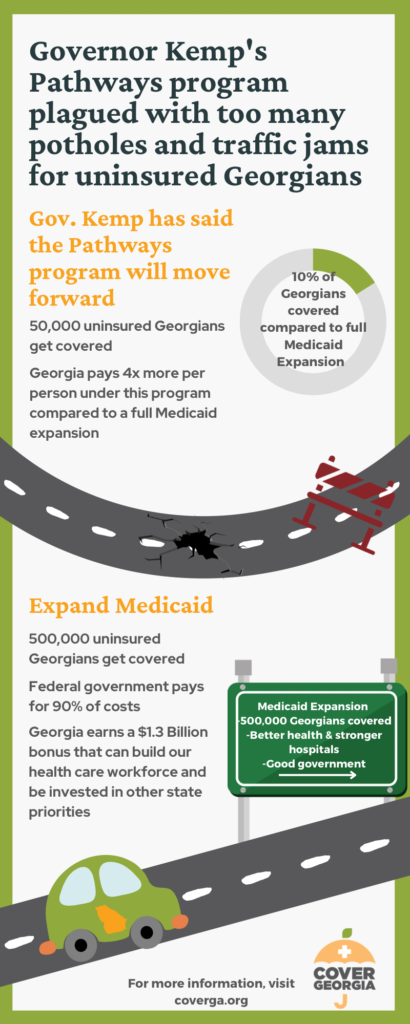

Pathways is a complicated program with many rules and restrictions, so we expect only a fraction of eligible Georgians will get covered through the program. The Governor and his administration have estimated that between 31,000-100,000 Georgians will be able to enroll in Pathways. (Full Medicaid expansion would cover more than 400,000 Georgians.)

Some people who are likely to be left out include:

- Stay-at-home parents

- Caregivers for aging family members or children with a disability

- People in mental health or addiction recovery programs

- Rural residents and people of color who live in areas where good jobs are hard to find

- People who do not have reliable internet access or a car

These folks may not meet the requirements for Pathways or won’t be able to keep up with the tedious monthly reporting. They will likely be left behind.

Medicaid expansion: an easier, better solution

Pathways is a broken bridge that lets too many Georgians and too much money fall through the cracks. Because of its complications and restrictions, thousands of Georgians will remain uninsured, and our state’s tax dollars–which are meant to help families access health care and keep hospitals open–will sit unused in Washington, D.C.

Georgians deserve better. We deserve access to affordable, quality health care regardless of how little money is in our wallets. We deserve healthy hospitals whose doors are open to care for their communities. We deserve to visit the doctor when we’re sick and fill a prescription without worrying about whether to pay our rent or the medical bill.

Luckily Georgia leaders can replace Pathways with a program that is simpler, covers more people, costs less per person, and meets our state’s needs: Medicaid expansion!

How you can help

Here are some things you can do to get Georgians covered and keep up the calls for Medicaid expansion:

- Spread the word about Pathways. Tell the uninsured Georgians in your life about the program and encourage them to apply. Here is some helpful information to print and share:

- Uninsured in Georgia? flier

- Information about Pathways from the Georgia Department of Community Health

- If you apply for the Pathways program, tell us about it! We want to know if you got covered or were turned away. Record your story and enter a monthly $100 give away, sponsored by our partners at Vocal Video! GHF is committed to directly compensating select storytellers with electronic gift cards!

- If you are helping people enroll in Pathways, we want to hear from you too!

- Speak up for Medicaid expansion! Ask the Governor and our state legislators to expand Medicaid when they return to the state Capitol in January 2024.

- Don’t know what to say? We’ve got you covered. Here are some fast facts about Medicaid expansion that you can use to write or call your state leaders.

By working together, we can make sure that all Georgians–regardless of how much or little money they have–have health coverage and the access to care that comes with an insurance card.

Cover Georgia celebrates the 58th anniversary of Medicaid this Sunday, July 30th! Fifty-eight (58) years ago Medicaid was signed into law and since then has worked to provide affordable health care coverage to low-income children and families, pregnant people, people with disabilities, and seniors. One of Medicaid’s biggest lifetime achievements has been to narrow racial disparities in health care access all across the country.

In 2019, Gov. Brian Kemp proposed a plan that would limit new Medicaid coverage to a much more restricted number of Georgians. The Governor’s plan would impose debunked “proof of work” requirements and require unaffordable premiums for some enrollees. The Trump administration approved the complete plan in 2020. In December 2021 the Biden administration changed its approval to disallow the burdensome work requirements and premiums. You can read more about the back-and-forth over the Governor’s plan in this blog and on our waiver timeline.

Background

In 2019, Georgia put forward a plan to expand Medicaid to a limited group of Georgians. Under the “Georgia Pathways” plan, the state would allow adults with incomes below the poverty line ($12,880 for an individual and $17,420 for a family of 2) to qualify for Medicaid health insurance. The Georgia Pathways plan also required these newly eligible adults to complete and document 80 hours of work (or other “qualifying activities”) each month to enroll in and keep their coverage. Some enrollees would also be required to pay a monthly premium to stay covered.

In 2020, the Trump administration approved the Pathways plan and implementation was set to begin in the summer of 2021. However, when the Biden Administration took over in the spring of 2021, they paused the approval to allow the new administration more time to review the Pathways plan. The Biden administration was particularly interested in the work requirements and premium payments and whether these additions violated the spirit and goals of the Medicaid program.

At the end of 2021, the Centers for Medicare and Medicaid Services (CMS) approved the Georgia Pathways plan, allowing Georgia to extend Medicaid coverage to Georgians making up to the poverty line (or 100% FPL). However, CMS denied the state’s request to include work requirements and premium payments as a condition of enrolling in and maintaining Medicaid coverage. CMS cited concerns about the devastating impact the COVID-19 pandemic has had on both the health and economic security of Georgians as the reason for denying these provisions. You can learn more about the Georgia Pathways program and the approval timeline here.

Recent Updates

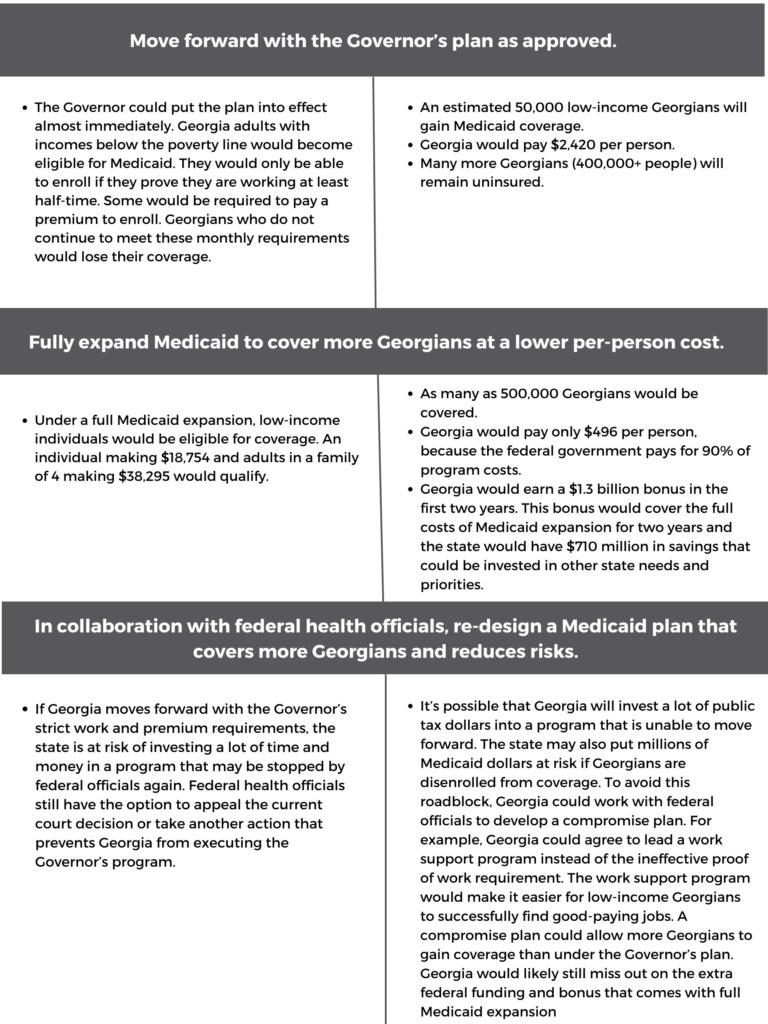

Following this final approval of the Pathway’s plan and denial of the request to include work requirements and premium payments, Governor Kemp was left with four options. He could do nothing and continue to let low-income Georgians remain uninsured, appeal CMS’s decision, implement the Pathways waiver without the work and premium requirements, or fully expand Medicaid to cover as many as 500,000 low-income Georgians (you can learn more about the options available following the waiver approval here). Governor Kemp chose the second option and appealed CMS’s decision to deny the inclusion of work requirements and premium payments.

In August 2022, a judge issued a ruling on the appeal of CMS’s decision. The judge ruled that the Biden Administration could not deny the previously approved work requirements and premium payments from the original Georgia Pathways plan. This decision means the state can move forward with implementation of the waiver as originally approved in 2020. CMS has yet to respond to this ruling, but does have the option to appeal the decision to a federal appeals court.

What does this court decision mean for Georgians?

Governor Kemp can carry out his Medicaid plan as he intended. If the program goes into effect, Georgia adults with incomes below the poverty line would become eligible for Medicaid. They would only be able to enroll if they complete monthly paperwork to prove they are working at least half-time. Some would also be required to pay premiums. Governor Kemp’s administration estimates that only about 50,000 Georgians (out of 500,000) would successfully gain coverage.

Most otherwise-eligible Georgians will be unable to enroll in or keep their Medicaid coverage because of the work requirements or premium payments.

The work requirements do not work for many uninsured Georgians. Georgians who are full-time caregivers, people in mental health & addiction recovery programs, and people living in areas where good jobs are harder to come by would not meet the work requirements. That means rural residents, people living in low-income communities, and communities of color are more likely to be left uninsured.

Georgia leaders can choose a better path

With this most recent court decision, Governor Kemp and the Georgia legislature once again face a choice about how to best connect low-income Georgians to health coverage and care.

Their options are:

Medicaid expansion is still the best option for Georgians

Full Medicaid expansion still makes the most sense for Georgia. Medicaid expansion would boost the health of Georgians by increasing early detection for diseases like cancer and heart disease. The expanded coverage would relieve the burden on rural hospitals, ensuring that their communities continue to have access to care. Medicaid expansion would close long-standing health gaps that unfairly cut short the lives of Black and brown Georgians.

Too many Georgians have been left without coverage for far too long. Our state leaders must choose the best way forward for our state. Medicaid expansion is the best way forward.